The entrepreneurial journey often includes relentless hustle, lean budgets, and the constant pursuit of the next milestone. Then, sometimes, the landscape shifts dramatically. A successful acquisition, a major funding round, or even an unexpected windfall can flood your personal and professional life with sudden liquidity.

While the initial elation is understandable, this pivotal moment requires careful navigation. Mishandled, sudden wealth can become a source of stress and regret.

This article provides a road map for entrepreneurs stepping into this new financial reality.

Start by Doing Nothing (Sort Of)

Even if you feel the urge to make big decisions, resist! The immediate aftermath of a significant liquidity event is often emotionally charged.

Allow yourself a brief period to decompress and acknowledge the accomplishment. Avoid making any major financial commitments in the first few weeks or even months.

Revisit the Buckets

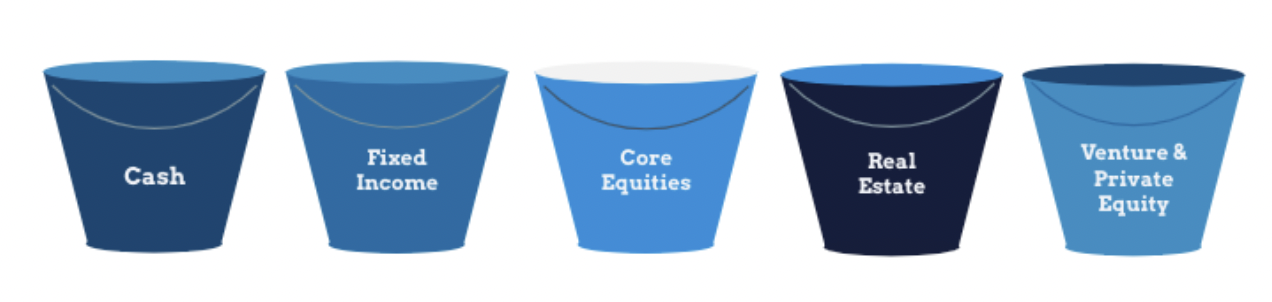

We structure wealth using our 5-Bucket Strategy: Cash, Fixed Income, Core Equities, Real Estate, and Venture/Private Equity. It’s how we manage our own money and how we help clients create balance across risk and liquidity.

Take a look at a quick snapshot of the five buckets we utilize:

- Bucket #1 – Cash: This bucket holds highly liquid funds for short-term needs, emergencies, and preserving capital with minimal risk.

- Bucket #2 – Fixed income: This bucket provides a relatively stable stream of income and acts as a portfolio diversifier through investments in bonds and other debt instruments.

- Bucket #3 – Core equities: This bucket focuses on long-term growth through investments in a diversified portfolio of publicly traded stocks.

- Bucket #4 – Real estate: This bucket encompasses tangible property investments aiming for income generation and potential capital appreciation.

- Bucket #5 – Venture and private equity: This bucket targets potentially large returns through investments in non-public companies, accepting significant illiquidity and risk.

Here’s how a liquidity event typically plays out using the 5 buckets:

- Your business was Bucket #5 (illiquid, high-growth).

- You sell, and now everything is in Bucket #1 (cash).

- The task is to carefully refill Buckets #2 through #4 by asking questions like:

- What needs to stay liquid to fund my life?

- What can be deployed into cash-flowing investments?

- What portion should remain flexible for opportunistic plays?

Name a “No” Person

Liquidity events don’t stay quiet. They tend to be public, especially with business sales or IPOs. Suddenly, you might find yourself inundated with requests: investment opportunities, charitable solicitations, and loans from friends and family. While it’s natural to want to be helpful, saying “yes” to everything can quickly deplete your resources and lead to resentment.

You need someone in your corner whose job is to say no—or at least, pause—to those inbound pitches. We often play that role for our clients, offering an objective perspective that can help you filter out unsuitable opportunities and navigate potentially awkward social situations.

Build Your New Paycheck

If your business was your income, selling it means that income is gone. You need to ask:

- What’s my new earn rate?

- What investments replace my paycheck?

You may have capital, but capital doesn’t replace cash flow unless it’s positioned to do so. That’s where investing in income-producing strategies comes in. Real estate, dividends, alternative income strategies like Solidarity Capital —these aren’t flashy headline-makers, but they help cover the daily expenses that don’t stop just because your cap table did.

It’s common for entrepreneurs to keep chasing growth. But it’s worth balancing that with cash flow so you don’t feel forced back into the grind before you’re ready.

Leverage Your Industry Knowledge

One of the often-overlooked upsides of being an entrepreneur is that your experience creates access. When you’ve built a business in a specific industry—whether it’s healthcare, manufacturing, or software—you’ve developed a deep network and subject-matter expertise that other investors don’t have. That’s a meaningful advantage when it comes to private deal flow.

You may not want to run a company day to day anymore, but you’re still seen as an expert in your space. That reputation draws opportunities. People will want you on advisory boards, in investor circles, or as a sounding board.

Just make sure the opportunity is a fit for you, not just the deal. And be cautious about how many roles you say yes to. We often remind clients that some invitations are less about investing capital and more about donating time.

Plan the Fun

Yes, you’re going to want to celebrate. And you should. But be honest about it.

Are you buying a G-Wagon or a Gulfstream? Is this about a one-time splurge, or a shift in lifestyle expectations? These decisions aren’t inherently good or bad. But they are financial. And they belong in the plan, not as guilt-inducing line items, but as part of the bigger picture.

Build a “fun budget” into your plan. Acknowledge the need to blow off some steam. But don’t let the celebration run away with the capital you worked so hard to unlock.

Psychological Shift

You gave away your baby. Now what?

There’s a psychological shift that happens when the business no longer needs you. It can feel disorienting, even when the bank account looks great. Many of our clients find they need time to rediscover who they are without the title, the team, or the grind.

That’s normal. And it’s okay.

The smartest advice we can offer is simple: don’t rush. Use the buckets. Find your “no” person. Put your industry knowledge to work. Build structure before jumping into the next thing.

And when you’re ready to talk through what’s next, we’re here.

Take the Next Step

Sudden liquidity is a transformative event, offering both immense opportunity and potential pitfalls. By approaching it with intention, seeking professional advice, and staying grounded in your values, you can navigate this new chapter successfully.

When you’re ready to see what wealth management can do for you and your newfound wealth, reach out to our team at info@solidaritywealth.com or call 385-374-1665 to schedule a discovery call.

About Jeff

For over a dozen years, Jeff McClean has advised some of the country’s most successful families on all aspects of their wealth. With his background as a former tax and estate planning attorney at a prominent Houston, Texas, law firm, Jeff has advised clients through business sales, funding rounds, IPOs, complex tax and wealth planning transactions, private and public market investments, executive compensation packages, succession planning, and much more. In short, Jeff helps clients navigate the unique challenges that come with building wealth and helps them better predict their financial future.

In addition to co-founding Solidarity Wealth, Jeff advises single-family offices on a broad array of challenges. He also serves as the Managing Partner of Solidarity Capital, an income fund managed separately by the Solidarity partners.

Jeff is a sought-after thought leader on a wide range of tax, finance, and estate planning topics. Jeff has appeared on CNBC, Bloomberg, and Fox Business, has been quoted in Barron’s, Kiplinger’s, and Yahoo!Finance, has published in diverse publications from Silicon Slopes Magazine to the Taxation of Exempts Journal by Thomson Reuters, and spoken to endless professional groups and large company conferences.

Jeff holds a bachelor’s degree in accounting from Brigham Young University – Idaho and a Juris Doctor, with honors, from the University of Texas School of Law. Outside of work, Jeff is married and the father of three amazing children. He has also served as past president of the Salt Lake Estate Planning Council.

About Zach

Zach Whitchurch is the President and a wealth advisor at Solidarity Wealth, a privately held, independent wealth management firm that serves as a multi-family office to some of the Mountain West’s most successful families, technology entrepreneurs, and executives. Zach works with clients to develop both “Wealthy Financial Habits” and “Healthy Financial Habits” and thrives on helping them understand their finances by simplifying the complex. He uses his broad knowledge on a wide variety of topics to implement creative strategies for clients as he helps them feel both seen and heard, and supports them along the path to their dreams.

Zach has a bachelor’s degree in accounting and a master’s degree in finance from the University of Utah and holds the CERTIFIED FINANCIAL PLANNER® and Certified Private Wealth Advisor® designations. He is also a Managing Partner of Solidarity Capital. Outside of work, Zach enjoys spending time with his wife and four children and being active in both indoor and outdoor sports. He is also involved with coaching youth sports, and loves to read and learn about how the world works on a deeper level.

Solidarity Wealth is a registered investment adviser. This material is solely for informational purposes. Advisory services are only offered to clients or prospective clients where Solidarity Wealth and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Solidarity Wealth unless a client service agreement is in place.