By Zach Whitchurch

President | Wealth Advisor

Certified Private Wealth Advisor®

CFP®

In the finance realm, we often encounter complex strategies and intricate market analyses. However, one of the most powerful concepts in wealth building is also one of the simplest: consistency. This principle, instilled in me from a young age, has proven to be a cornerstone of financial success for many of the affluent individuals and families we serve at Solidarity Wealth.

The Seeds of Financial Wisdom

My journey with saving began in childhood, sparked by my parents’ simple yet profound advice: “Make sure you’re saving at least a little bit of money.” I vividly remember when I was about 10 years old, my dad told me and my brother that someone at his company needed help. Curious, we asked what kind of help they needed. To our surprise, the task was to “count cars” at a particular intersection. For an hour of diligent car-counting, I earned $10 in cash—and I felt like a superhero!

This early taste of earning sparked a passion for work and saving that would shape my future. Throughout my childhood, I took on all sorts of jobs: delivering newspapers, pulling taffy, working construction—you name it, and I probably have some experience with it. Each job, no matter how small or unusual, was an opportunity to earn and (more importantly) to save.

My parents’ mantra of “save your money” echoed through every paycheck, big or small. I’d dutifully make trips to the First Interstate Bank near our house, depositing a few dollars here and there. When my savings reached $300, I felt like the richest kid in the neighborhood. Looking back, that feeling of accomplishment and security from having savings, however modest, was an invaluable lesson.

As a 10-year-old, feeling wealthy with $300 in the bank might seem quaint now. However, that early experience laid the foundation for a lifelong habit of consistent saving—a habit that has served me well and one that I now emphasize to our clients at Solidarity Wealth.

These childhood lessons in consistently saving small amounts have taken on new meaning as I’ve progressed in my financial career. What started with pocket change and modest paychecks has evolved into a deep understanding of one of the most powerful forces in finance: compounding.

Compound Interest: The Entrepreneur’s Ally in Wealth Building

Just as my small, regular deposits added up to $300—a fortune in a child’s eyes—consistent saving and investing over longer periods can lead to even more impressive results. To illustrate this, let’s consider a hypothetical scenario.

Imagine an individual who, inspired by early lessons in saving, began setting aside $1,000 per month in 2004 and maintained this practice for 20 years. The total amount saved would be $240,000—already an impressive sum. However, where and how this money is invested can significantly impact the final result.

Cash/Money Market Fund: If this sum were placed in a conservative investment vehicle, such as a money market account, it might have grown to approximately $295,000 over 20 years. This represents a safe, low-risk option but demonstrates minimal growth due to the lower interest rates typically associated with cash investments.

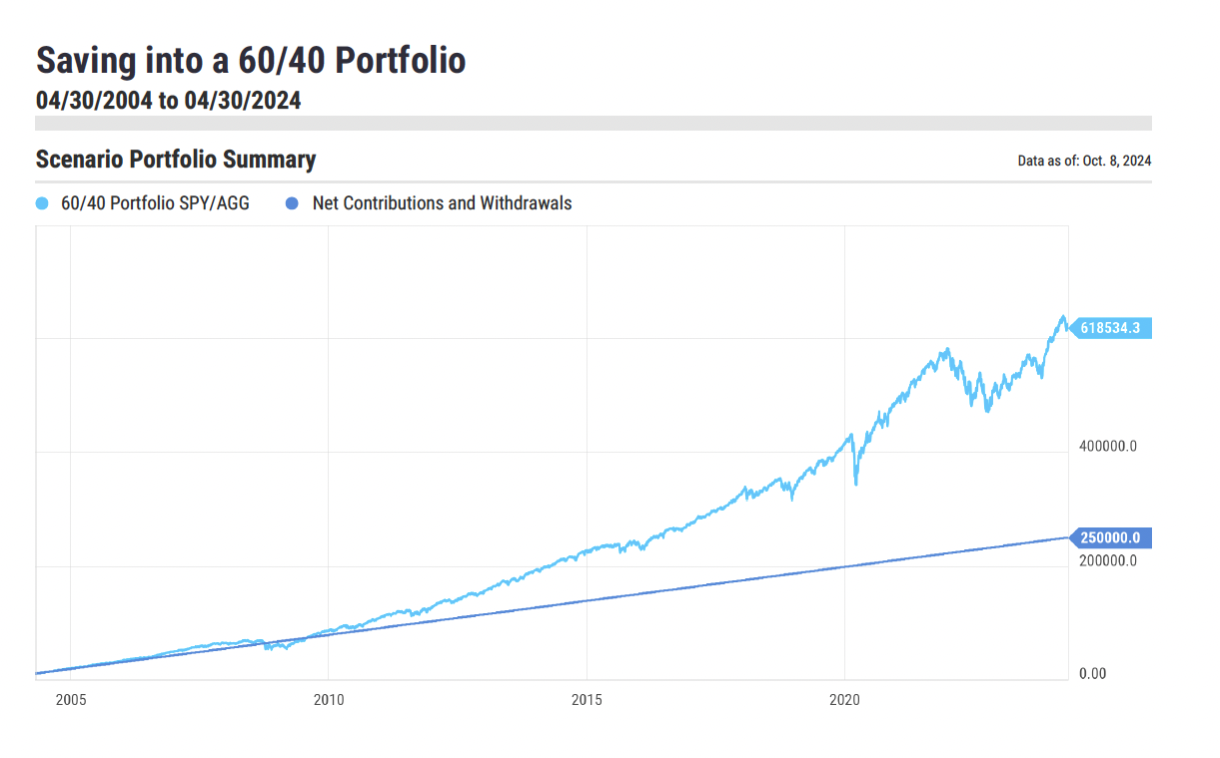

Balanced 60/40 Portfolio: A more balanced approach, such as a well-diversified portfolio composed of 60% equities (represented by SPY) and 40% fixed income (represented by AGG), could have produced a more substantial outcome. Historical market performance suggests this strategy might have resulted in a total of approximately $635,000. This demonstrates the benefit of balancing risk with the stability provided by bonds while still participating in the growth of the equity markets.

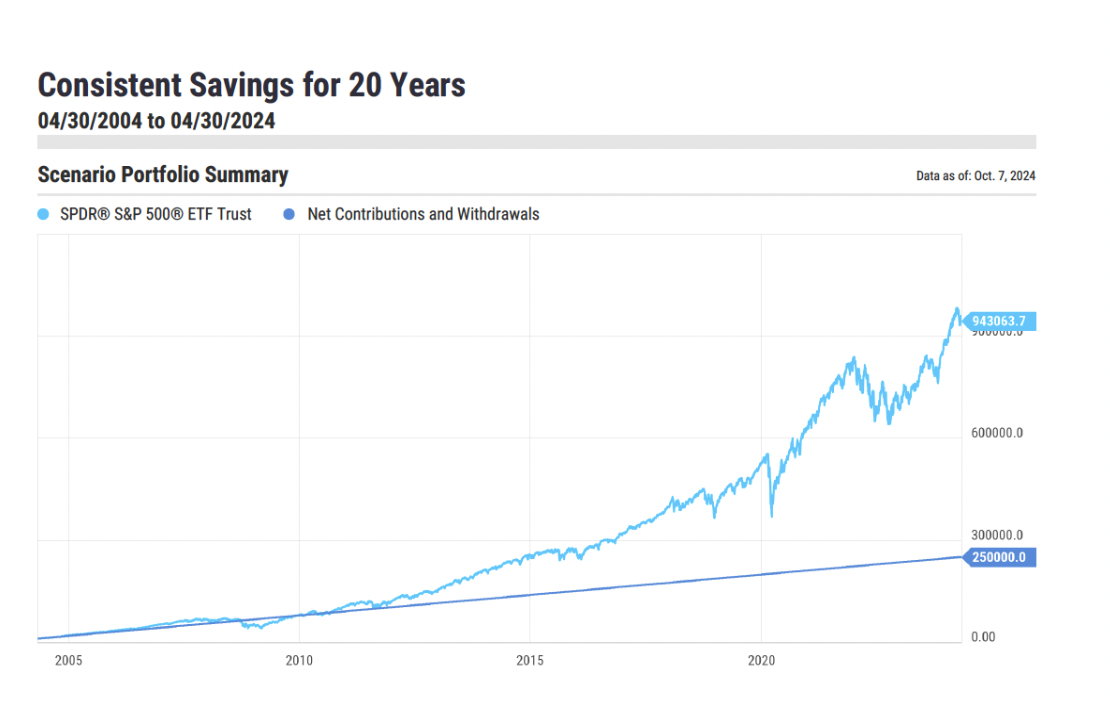

100% Equity Portfolio: Lastly, an all-equity portfolio that tracks the S&P 500 index, while considered more aggressive, would have potentially resulted in a much larger sum. Based on historical performance, a 100% equity portfolio could have grown to around $943,000. While this offers the highest potential for growth, it also comes with increased volatility and is best suited for those with a higher risk tolerance.

This stark difference underscores the profound impact that early guidance in investing can have. Having someone in your life—a parent, a mentor, or a trusted advisor—who helps you start investing at a young age can be transformative. They not only teach you the mechanics of investing but also instill the confidence to navigate financial markets over the long term. This early exposure to investing concepts can lead to decades of compound growth, potentially resulting in significantly greater wealth accumulation over time.

Balancing Business Reinvestment and Personal Wealth Growth

For many of our entrepreneurial clients, the idea of setting aside funds for savings or investment can be challenging. There’s often a temptation to reinvest all available capital back into the business. It’s not uncommon to hear entrepreneurs say, “All my extra dollars are going to fund my company. I will plan to save when I actually have extra cash!”

This mindset, while understandable, can lead to missed opportunities for personal wealth building. While reinvesting in your business is crucial for growth, it’s equally important to maintain a balanced approach to personal finance.

As businesses flourish and personal income increases, new financial demands often arise. From upgrading vehicles to funding children’s activities or expanding living spaces, the competition for those hard-earned dollars intensifies. Ironically, when that “extra cash” finally arrives, entrepreneurs often find that the demands on their resources have grown proportionally, making it just as challenging to start saving.

This is where the discipline of consistent saving becomes paramount. By treating personal savings as a non-negotiable expense from the outset—effectively “paying yourself first”—entrepreneurs can build significant personal wealth over time, even as other financial obligations increase and they continue to invest in their businesses.

The Importance of Scaling Your Savings

As your income grows, consider proportionally increasing your savings rate. This approach helps mitigate the effects of lifestyle inflation and allows you to capitalize on your higher-earning years.

Navigating Market Volatility: A Long-Term Perspective for Business Owners

One of the most challenging aspects of long-term investing is navigating market volatility. It’s natural to feel concerned when the value of your investments drops below your initial contribution. However, maintaining a long-term perspective can help view these moments as opportunities rather than setbacks.

The COVID-19 pandemic provides a powerful example of this principle in action. In early 2020, as the pandemic unfolded, global markets experienced a sharp downturn. An investor who had put $100,000 into a diversified investment account just before this event might have seen their portfolio value drop significantly in a matter of weeks. At that moment, it may have felt like the worst financial decision they had ever made.

However, those who maintained their long-term perspective and stayed invested—or even better, continued to invest during the downturn—were well-positioned to benefit from the subsequent market recovery and growth. What initially seemed like a financial setback turned into an opportunity to acquire assets at lower prices, potentially enhancing long-term returns.

This real-world example illustrates a crucial point: market volatility, while uncomfortable, can present opportunities for long-term investors. By viewing your $100,000 investment as the beginning of a long series of contributions rather than a one-time event, you can reframe market downturns as chances to make your next purchases at more favorable prices.

This perspective shift from “trading” to “investing” can profoundly impact how you approach market fluctuations. Instead of fearing volatility, you can learn to see it as a natural part of the investing process—and potentially even as an ally in your long-term wealth building journey.

The Discipline of Consistency

Whether you’re an established entrepreneur or just beginning your wealth-building journey, the key lies in establishing a plan and adhering to it consistently. While the path may not always be smooth, staying committed to your saving and investing strategy can potentially lead to significant long-term benefits.

At Solidarity Wealth, we work closely with our clients to develop personalized strategies that align with their unique goals and risk tolerances. We believe that by fostering wealthy habits—including consistent saving and thoughtful investing—we can help our clients work toward their financial objectives and create lasting legacies.

Remember, true wealth extends beyond mere numbers. It encompasses the impact you can make, the legacy you can leave, and the peace and confidence that comes from knowing you’ve taken proactive steps toward your ideal financial future.

Schedule a consultation with Solidarity Wealth to discuss how our tailored wealth management strategies can support your long-term financial goals. We invite you to reach out at info@solidaritywealth.com or call 385-374-1665. Let’s discuss how we can help you cultivate wealthy habits that may serve you well for years to come.

About Zach

Zach Whitchurch is the President and a wealth advisor at Solidarity Wealth, a privately held, independent wealth management firm that serves as a multi-family office to some of the Mountain West’s most successful families, technology entrepreneurs, and executives. Zach works with clients to develop both “Wealthy Financial Habits” and “Healthy Financial Habits” and thrives on helping them understand their finances by simplifying the complex. He uses his broad knowledge on a wide variety of topics to implement creative strategies for clients as he helps them feel both seen and heard, and supports them along the path to their dreams.

Prior to co-founding Solidarity Wealth, Zach was a financial advisor and a senior vice president of investments at Wells Fargo. He has a bachelor’s degree in accounting and a master’s degree in finance from the University of Utah and holds the CERTIFIED FINANCIAL PLANNER® and Certified Private Wealth Advisor® designations. He is also a Managing Partner of Solidarity Capital. Outside of work, Zach enjoys spending time with his wife and four children and being active in both indoor and outdoor sports. He is also involved with coaching youth sports, and loves to read and learn about how the world works on a deeper level.

Solidarity Wealth is a registered investment adviser. This material is solely for informational purposes. Advisory services are only offered to clients or prospective clients where Solidarity Wealth and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Solidarity Wealth unless a client service agreement is in place.