By Danny Clark, CFP®, Certified Private Wealth Advisor®

Not long ago, I met with a client who earns well into the six figures. By any measure, she’s successful. But during our conversation, she said, “I feel like I’m struggling financially.” That comment isn’t unusual. In fact, I hear it more often than you’d expect, especially from professionals in their peak earning years.

You’re making the most money you’ve ever made, yet you don’t feel wealthy. If you feel broke despite making good money, you’re not alone. You look at your checking account and wonder how someone with your income can feel cash-strapped.

The issue isn’t your income, it’s visibility. When you’re successfully saving and investing across multiple financial vehicles, it can feel like your money is disappearing rather than growing. You’re actually doing everything right, but it may not feel that way.

Where Your Money Is Really Going

When we dug into this client’s cash flow, we discovered she was allocating nearly 35% of her gross income toward long-term financial goals—retirement accounts, equity investments, real estate, and more. That’s outstanding but it also explains why her checking account felt tight.

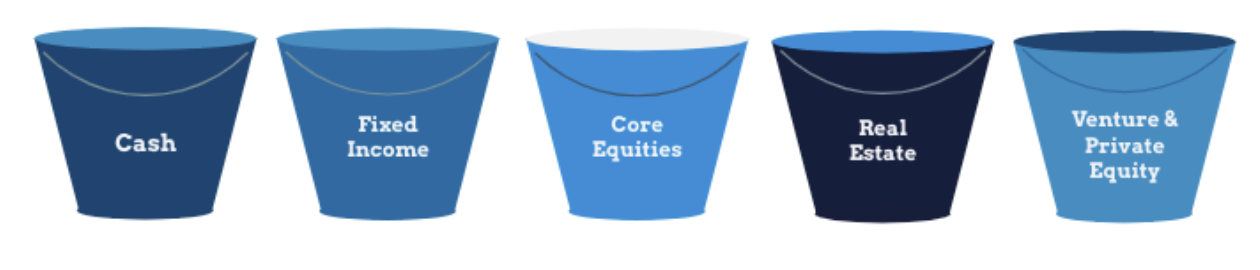

At Solidarity Wealth, we often walk clients through what we call the Five-Bucket Reality Check. It’s a framework that helps explain where your money is going and why it feels like it’s disappearing.

Bucket Breakdown

The breakdown usually looks something like this:

Bucket 1: Cash—your emergency fund and short-term liquidity needs

Bucket 2: Fixed income—bonds and stable investments providing steady returns

Bucket 3: Core equities—your diversified stock portfolio for long-term growth

Bucket 4: Real estate—both your home and investment properties

Bucket 5: Venture capital and private equity—higher-risk, higher-reward investments

When you add retirement accounts like your 401(k), HSA contributions, and 529 education savings on top of these five buckets, you can see why your paycheck feels stretched thin despite strong earnings.

Why High Earners Feel Broke: The Hidden Pressure

This is particularly challenging for professionals in expensive markets like Park City, where housing costs are significant and childcare can run well past $50,000 annually in some cases. You’re competing with high expenses while simultaneously funding multiple long-term financial goals.

The problem isn’t your cash-flow management, it’s the psychological disconnect between earning well and feeling wealthy. You’re building substantial assets, but they’re invisible in your day-to-day experience.

3 Ways to Stop Feeling Broke When You Make Good Money

The solution starts with visibility and intentionality. First, create a monthly snapshot that shows all five buckets. See your total contributions across all categories; this reveals your true savings rate and financial progress.

Second, build in what I call conscious lifestyle spending. After funding your five buckets, deliberately allocate money for experiences and purchases that enhance your current quality of life. It’s not irresponsible, it’s sustainable cash-flow management.

Third, remember that this feeling is temporary. As your income grows and some expenses decrease (children age out of daycare, mortgages get paid down), you’ll have more flexibility while maintaining these strong financial foundations.

Feeling cash-strapped while earning good money can sometimes indicate you’re making smart long-term financial decisions, not poor ones. The key is creating systems that give you visibility into your progress and intentional permission to enjoy your current success while building future wealth.

Making It Work for You

Does this situation sound familiar? Don’t forget that you’re not alone, and you’re likely doing better financially than you realize. For professionals in the area who want to gain clarity on their cash flow and build a comprehensive financial strategy, I’d welcome the opportunity to review your complete financial picture. Reach out to me at info@solidaritywealth.com or call 385-374-1665 to schedule a discovery call.

Remember, if you feel broke despite good income, check your buckets. You might be surprised by what you find.

Frequently Asked Questions About Why You Feel Broke Making Good Money

Why do I feel broke even though I make six figures?

High earners often feel broke because they’re aggressively saving across multiple accounts: 401(k), HSA, 529s, taxable investments, and real estate. When 30-40% of your gross income goes toward wealth-building before you see it, your checking account naturally feels tight. You’re not broke; your money is just working for you in the background.

What’s a good savings rate for high-income professionals?

A savings rate of 20-30% of gross income is strong. If you’re hitting 35% or more like the client in this article, you’re in excellent shape. The challenge is balancing aggressive saving with enough lifestyle spending to enjoy your current success.

How do I know if I’m saving too much?

If you consistently feel stressed about daily expenses despite a high income, you might be over-saving. The goal is building wealth without sacrificing quality of life today. An experienced financial advisor can help you find the right balance between future security and present enjoyment.

About Danny

Danny Clark has a passion for serving successful families and making a positive impact in their lives. With over a decade of experience in the financial services and banking industry, he creates personalized retirement and financial plans for families to help them pursue their financial and family goals throughout their life. Danny’s experience in serving some of Park City’s most established families along with the deep experience, skill, and services of the Solidarity Wealth team allow Danny the opportunity to serve a growing number of successful families.

Prior to joining Solidarity Wealth, Danny served as a Wealth Advisor at another firm, and before that spent 12 years at Wells Fargo in Park City as a regional private banker. At Wells Fargo, Danny was responsible for developing lifelong relationships with families, while developing tailored banking, credit, and retirement solutions to help his clients be successful in their financial journey.

Danny has his bachelor’s degree in business management and holds the Certified Private Wealth Advisor® designation. He and his wife, Lindsay, are Park City natives and raising their own family. In his free time, Danny is an avid golfer and skier, and enjoys spending time with his family.

Solidarity Wealth is a registered investment adviser. This material is solely for informational purposes. Advisory services are only offered to clients or prospective clients where Solidarity Wealth and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Solidarity Wealth unless a client service agreement is in place.